Property, Tax and Finance Predictions for 2021

3483POSTED:

Articles by Matthew Gilligan.

After a crazy 2020, many investors and would-be investors are wondering what 2021 will hold in store for them. I outline my views and share my predictions in this article, which I hope you will find useful.

Firstly, who am I to tell you what 2021 might bring? As a brief background, I am a chartered accountant in public practice, based in Auckland. I spend most of my time working on my property portfolio and supporting our clients as the property partner at GRA (chartered accountants), where I am managing director. I would say I am no economist, but I am a businessman well engaged in property all over New Zealand. And I have spent 25 years as a chartered accountant, specialising in property investment.

I expect that 2021 will see more growth in property values, with another cracker of a year throughout the country. It takes a while for New Zealanders to wake up to a property boom, but once they get the bit between their teeth, sentiment overwhelms any rational investment analysis, and prices continue to rise. 2020 kicked off the growth, and it’s just getting going in my opinion. The damper on the growth, however, might well be LVRs reducing credit availability (more on this below). ANZ have just moved to 60% LVRs for investors voluntarily, following the Reserve Bank’s announcement that they will move to 70% LVRs next year. A reduction of credit always constricts market activity.

Talking of growth, while the media highlight social inequity and wealth disparity, and seek to lay the blame at investors' doors, the rest of us know that there is a lot more to property than landlords' greed and alleged tax perks. Low interest rates, supply shortages, loose LVRs, and huge inflows of migrants leading up to March 2020 have led us to where we are now. Media coverage and barbeque stories of existing investor success whip up FOMO (fear of missing out), pushing prices higher still. I see no real let-up in investor demand while borrowing remains cheap and largely accessible.

The 2020 boom isn’t all market sentiment and hysteria – there have been very real changes that have set us on this current upward portion of the property cycle. The most obvious is the reduction in interest rates, which has been the primary driver fuelling the booming New Zealand market.

PROPERTY & COVID

It was somewhat surreal to experience a general consensus among economists early this year that there would be a substantial drop in residential property prices and a huge recession as a result of Covid. They got it wrong.

In reality, almost the opposite happened, and the property market boomed throughout the country. While debate raged over what would happen and many (including quite a few valuers) predicted unprecedented mortgagee sales and market collapse, many New Zealanders were buying houses flat-out, looking at the windfall cash flow. A yield-driven boom is quite rational when you look at the cash flow coming off leveraged housing portfolios at present – as long as interest rates stay low. But with LVRs tightening, the mix of those that get to enjoy the benefit is shrinking to those with big deposits. So while there will be an investor appetite to buy, the market may be increasingly credit-starved.

2020 has delivered record-high prices in nearly all areas. When Auckland and main centres boom, price rises ripple to the rest of the country over time. It makes sense that the less affordable neighbouring towns and areas attract a population seeking a lower cost of living, through cheaper housing. I therefore expect ripple effect to continue to drive house prices higher in smaller centres and towns in 2021.

As we all know, houses are selling quickly at present – a median of 29 days to sell in November 2020, which is the fastest November sale time in 17 years – and listings are low. November 2020 listings were 18.7% down compared to 2019. (People are less likely to list and sell when they expect growth.) Five regions recorded their lowest ever inventory levels. The NZ median house price (excluding Auckland) was a record $615,000 in November, and the Auckland median hit a record $1,030,000 (REINZ data).

I expect this year’s property bull market to continue in 2021, unless changing LVRs starve investors of credit. LVRs will be a big issue in 2021 for investors.

Low interest rates providing unprecedented cashflow windfall to investors

To illustrate how lower interest rates improve the net operating income of a landlord, consider an example portfolio of three rentals with a cost of $1.5m and a net yield of 5%. (Net yield is rental income less operating expenses such as insurance, rates, maintenance and repairs). Deduct interest from net yield, and you have the net operating income (NOI).

In 2019, with interest rates at 5%, cash flow was merely breakeven on this example (5% net yield less 5% interest rate = $0 NOI). Now, with interest rates at 2.5% the same investment generates $37,500 in cash flow. There has been no underlying change in the investment, no additional cost incurred or rental increase. Such a windfall in liquidity for landlords is unprecedented in my experience in NZ property. And the flipside for homeowners is the same, with low rates improving affordability for all homeowners who borrow.

Lower interest rates really do drive housing demand, especially when borrowers can access credit. But will interest rates stay low? Most economists say they will for the foreseeable future, or the whole world will go broke.

Immigration

New Zealand experienced a historically high net inflow of people to the end of March 2020, and then barely 3500 migrants from April to October 2020 in the six months with Covid. Statistics NZ produce a fair bit of data, but I find it (at times) quite confusing. For example, Statistics NZ published an article saying the return of ex-pats is a myth, citing only a trickle of expats returning to the country. Yet pandemic response data says we have had over 84,000 people go through managed isolation into New Zealand to mid-December. Who are these people?

I find the presentation of the data fragmented and difficult to interpret, because it is hard to reconcile border crossings to intentions or outcome. But in Statistics NZ’s defence, it is hard to stratify people moving across a border, as their stated intention can be different to what they do, so there is a lot of estimating going on. Further, many are temporary workers or tourists.

While there will be a lag in getting quality data, which makes the current environment hard to read, I think that New Zealand will be a very popular migration destination once migrants are allowed back across our borders. This is due to our exceptionally successful Covid response and our internationally respected and high-profile Prime Minister. Anecdotally, I’ve dealt with quite a few people in the UK this year (through a business I have over there), and the English are all very quick to compliment New Zealand on our choice of PM and Covid response. I think we will once again be a hot destination for migrants post-Covid 19.

So long-term immigration might have crashed in NZ in 2020, causing the formation of new households to pause, but the flip side is this is allowing supply to catch up. That’s not a bad thing when you consider pent-up demand in the last decade in many of the regions. Have a look at the following graphs, modelling supply (building consents) against demand (household formation). I track this sort of data for my students and clients, on the basis that I encourage them to stick to areas in short supply. This reduces volatility in value when the property cycle goes into a downturn.

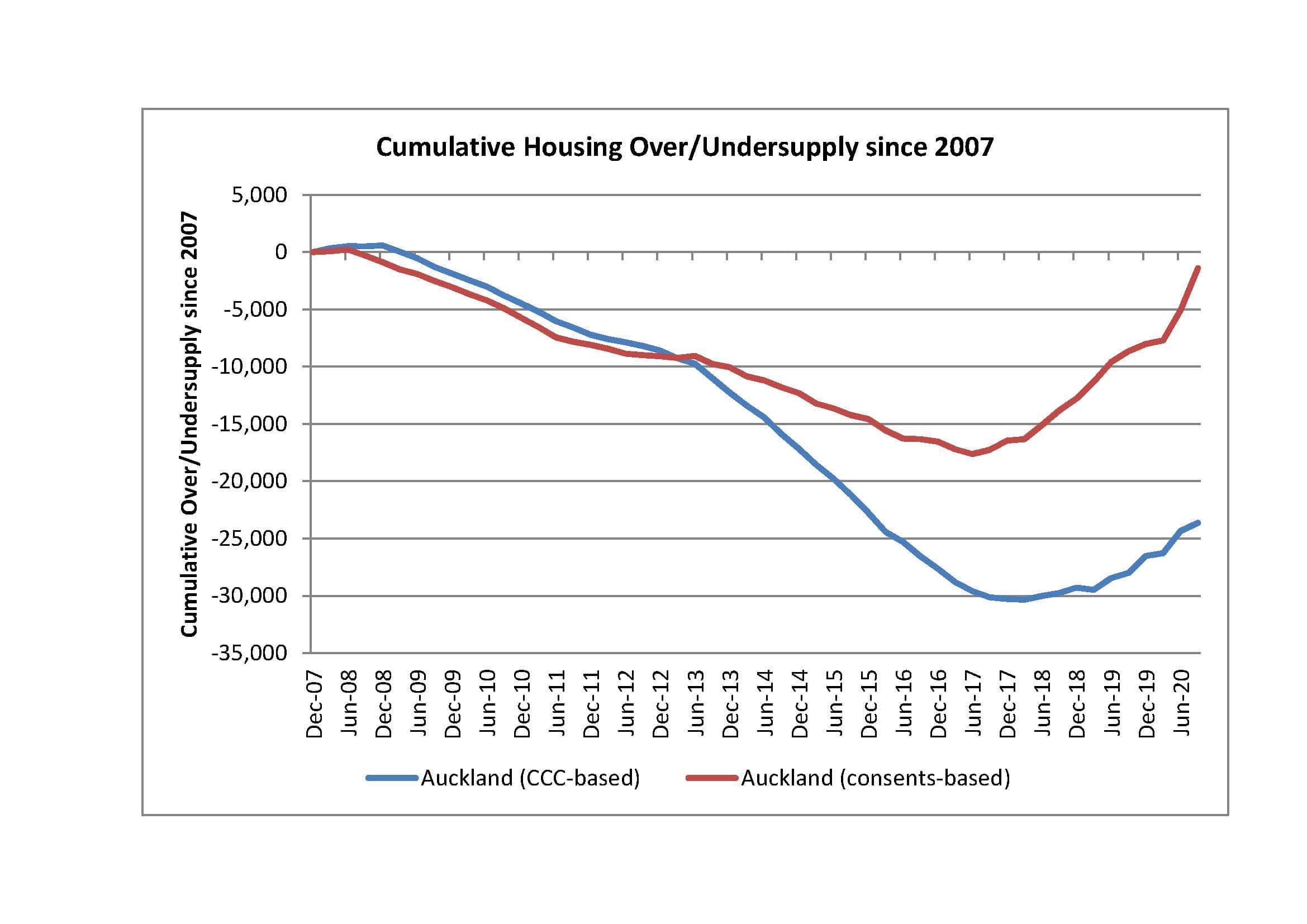

While in the last 10 years net migration has been so strong that it has far exceeded the supply of housing across New Zealand, Auckland has been starting to catch up on supply more recently. (Check out the red line in Graph 1 below, being building consents issued minus household formation [to reveal undersupply] over 10 years.) Aucklanders won’t feel this impact yet, because the red line represents houses in construction (consents). But once those houses in construction flush through into rental and housing stock, and if supply stays at current increased levels, we should see supply conditions ease in Auckland in the next couple of years. By my reckoning, Auckland is actually making enough houses now, with the very permissive zoning under the Auckland Unitary Plan. This narrative annoys a few property developers I know, as they like to believe that Auckland is forever supply starved. But I see that picture changing in the next 3+ years, particularly for units and terraced houses, where the bulk of Auckland supply is coming from now.

Graph 1 - Auckland over/under supply

Graph 1 - Auckland over/under supply

Source: www.gra.co.nz GRA ©

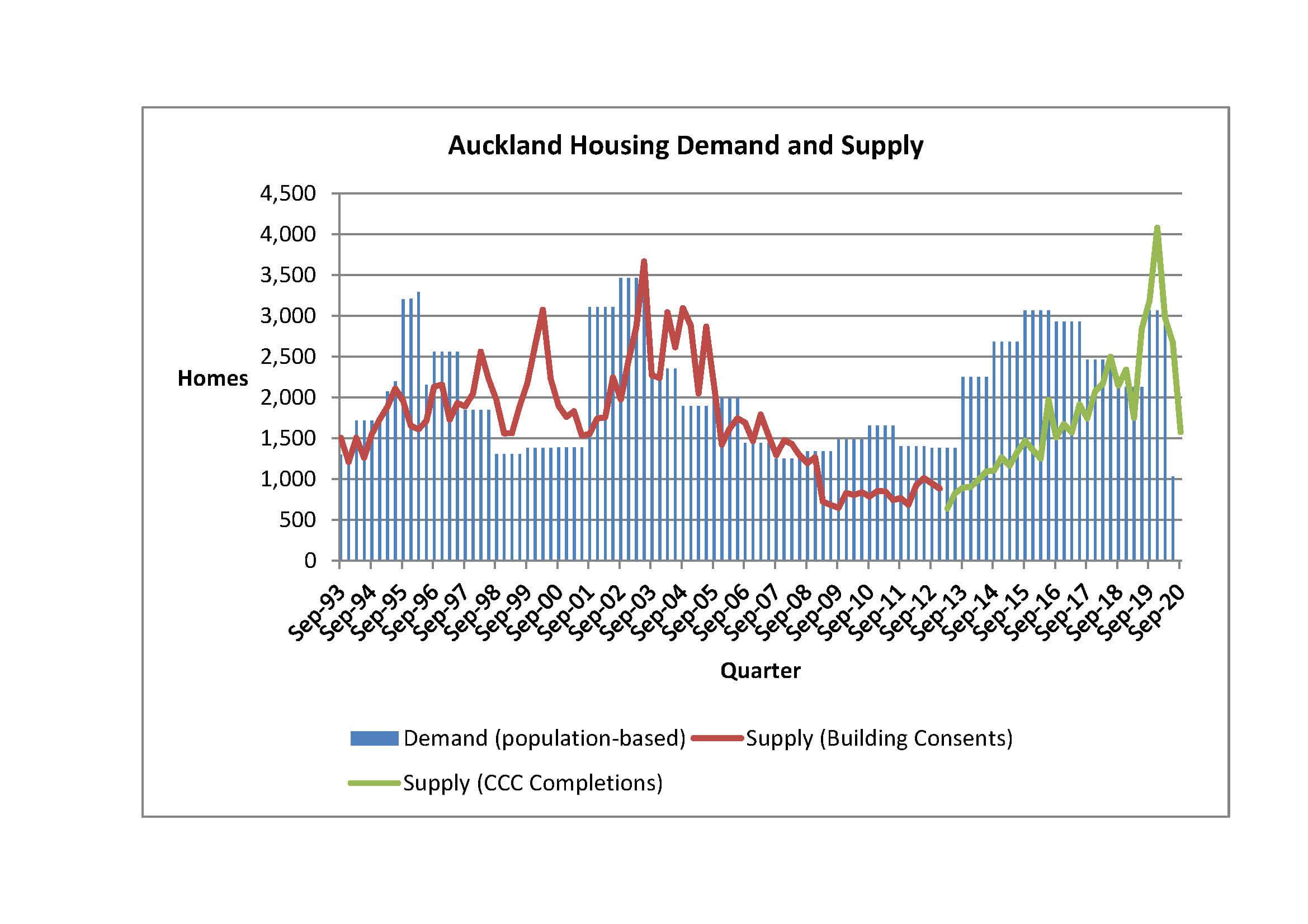

Graph 2 - Auckland supply versus demand to Sept 2020

Graph 2 - Auckland supply versus demand to Sept 2020

Source: www.gra.co.nz GRA ©

The blue bars in Graph 2 are household formation (assuming 3.2 people per house) and the red/green are housing supply. Code Compliance Certificate (CCC) data has only been available since 2013, so prior to that we have used building consents. In short, supply has vastly lifted, and in years to come it’s possible there could even be oversupply if the current conditions prevail. But hey, developers are rational, they will dial back construction once that happens, and who knows what migration will do. The key point is supply conditions are greatly easing in Auckland.

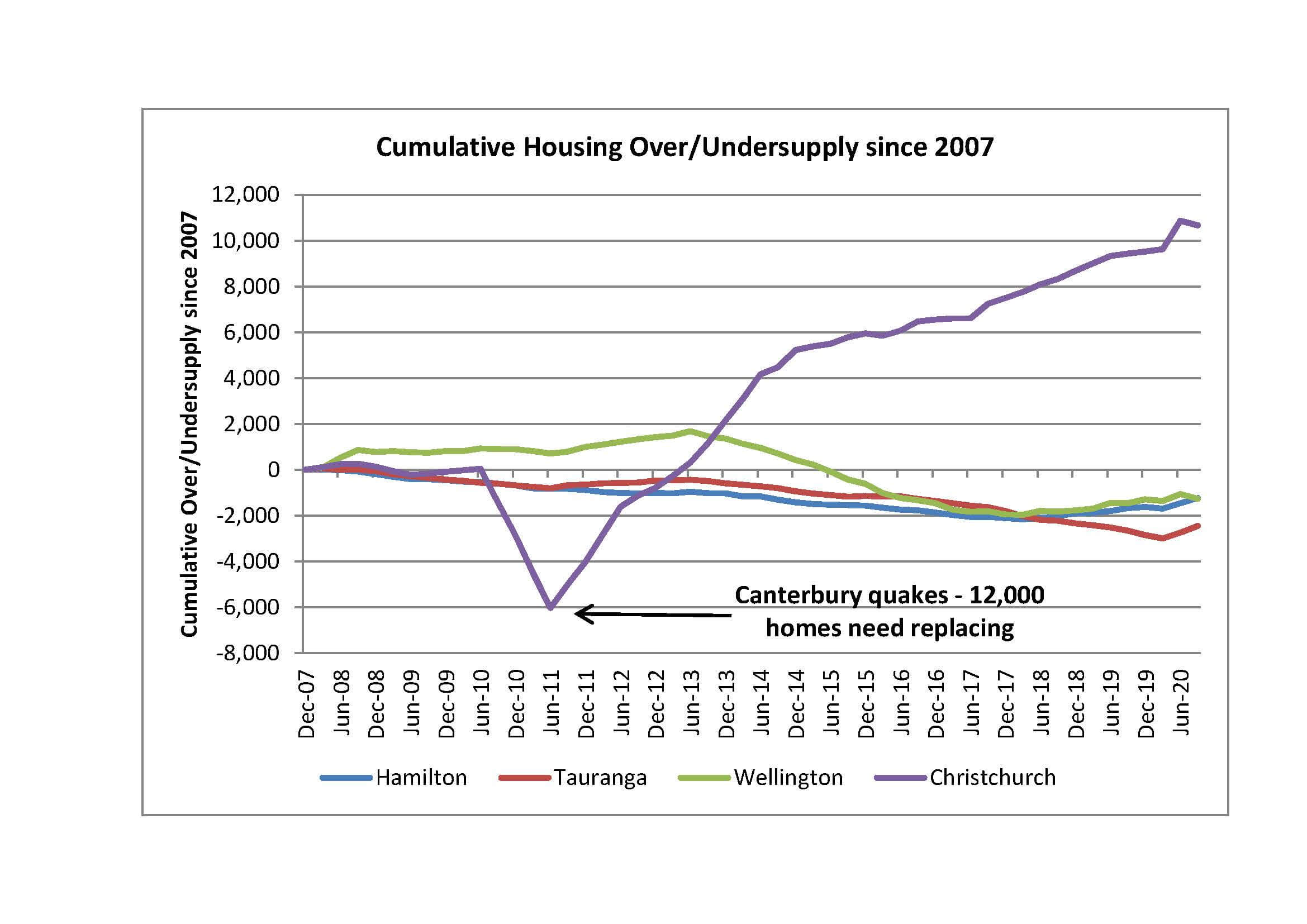

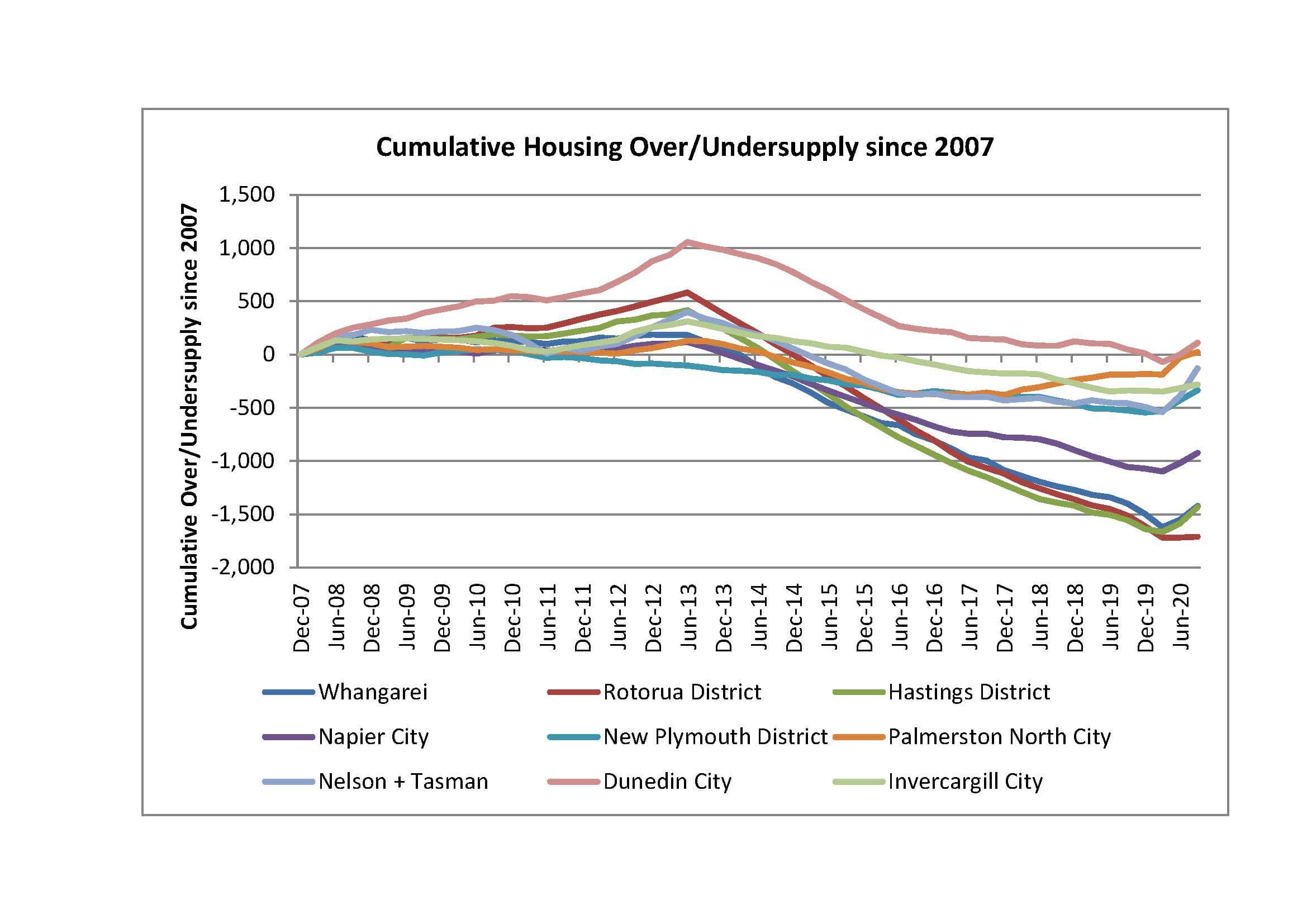

Main Centres & Regions

Where 10 years ago many small towns and centres in NZ were flush with housing, now the country is awash with people, following a decade of high migration (with the exception of post-Covid lockdown). Anecdotally, I speak to social housing providers and they are reporting their struggle to get houses in most places, not just in Auckland. Christchurch is the exception with looser supply.

Here are the cumulative housing supply graphs for the main centres. The small towns look much the same.

Graph 3: Cumulative Supply - Main Centres

Graph 3: Cumulative Supply - Main Centres

Source: www.gra.co.nz GRA ©

Graph 4: Cumulative Supply - Regions

Graph 4: Cumulative Supply - Regions

Source: www.gra.co.nz GRA ©

Due to page restrictions, I won't go on and dig too deep into the data, but note that we provide a lot of data to clients of GRA through our GRA Property School, if this is of interest.

TAX CHANGES

New top individual tax rate / Investor implications

With Labour winning the 2020 election, the top individual tax rate will be increased to 39%, probably from the 2021/22 tax year. The government has said that current tax rates for trusts (33%) and companies (28%) will remain unchanged, and hopefully, they will keep their word.

It therefore makes sense, if you are earning over $180,000, to own your assets with a taxable income in a company owned by a trust. The company tax rate is 28% until the profit is distributed, and if you declare a dividend to the trust, the top-up tax is just 5% (to get to 33%). On the other hand, it is an 11% top-up to distribute to an individual with a tax rate of 39%. Investors should be thinking about this sooner than later, in my view. Take advice from your tax adviser or talk to us at GRA (www.gra.co.nz).

It will be interesting to see if the government sticks to its word, and not introduce new taxes. The media cry for capital gains tax (CGT) or rifle taxes on property is at an all-time high. The Greens are baying for investor blood. Fingers crossed that Labour remembers what they promised New Zealand – a moderate approach to taxation and the status quo on CGT.

Chattels write-offs opportunity

A relevant tax change in 2020 is that one-off write-offs can be claimed for what would otherwise be depreciable chattels, if the total cost is less than $5,000 and the asset is purchased between 17 March 2020 and 16 March 2021.

With the Healthy Homes legislation, many landlords are installing air conditioning units, rangehoods and the like. This tax change represents a one-off opportunity to write them off, and is a significant increase on the previous low-value asset threshold of $500, and should be very helpful for property investors. The threshold drops back to $1,000 from 17 March 2021.

FINANCE

LVR restrictions

It was no surprise to see the RBNZ announce their consideration of reintroducing loan-to-value ratio (LVR) restrictions for property investors, to take effect from March 2021. Under their proposal, LVRs will likely move to 70% for investors but probably won't change for homebuyers. I don’t see this making much of a difference in 2021, as banks voluntarily moved to 70% in November 2020.

However, at the time of writing in mid-December, ANZ has announced they will voluntarily apply a 60% LVR to investor finances. This will slow housing in New Zealand, especially if the other banks follow this policy. (It's too soon to assess if they will.)

It would not surprise me to see the RBNZ revert to 60% LVRs for investment property lending for a while, to cool investor demand and lessen the rate of price increases. During the last boom in 2015/16, I recollect that an LVR of 70% did not slow the market that much, but a 60% LVR turned the lights out on property growth. A 40% deposit requirement really does stifle investors' ability to purchase, renovate, and recycle capital at pace. The reduction of leverage arrests market growth and can only be described as a bucket of ice on the property market.

I do think a conservative LVR is a more effective lever for the RBNZ to deploy than a higher Official Cash Rate (OCR), but it does favour those with greater wealth and equity. A higher OCR sucks cashflow from the economy and reduces available household income. I prefer to see household budget surpluses (which result from low borrowing interest rates) being spent in our economy. Investor-targeted LVRs will stifle investor demand, but leave owner-occupiers able to borrow more.

In the past, high OCRs have caused greater insolvency and hurt, whereas high deposit requirements for investor property simply reduce the number of people able to invest in property. This is much more preferable in my view.

Last comments: Tight LVRs push investors into the smaller towns, where they can still function with reduced capital. As LVRs tighten up, your deposit goes further on properties with a lower cost base.

Lower LVRs also drive investors to non-bank lenders who typically charge a 1% premium but lend to 80% LVR. (A non-bank lender is not regulated by the RBNZ.)

SUMMARY

While 2020 has been a remarkable year for investors, there is change on the horizon and we should be cautious of the implication of the changing banking environment.

I expect we will see a continuing property boom over the next 12 months, which makes it a good time to buy, all things being equal. The yield-driven boom is only getting started in my view, with interest rates being so low. However, LVRs may well become the stick in investors’ mud, starving them of access to capital. If we see ANZ’s 60% LVRs adopted across the board from banks voluntarily, or the RBNZ adopts 60% as the new LVR, that would be a game changer and the market will flat-line. Keep an eye on this, but consider a non-bank lender to take advantage of the market flattening, if that happens.

To learn more about the current property market and strategies that are effective, I invite you to attend GRA’s 7-module Property School course . Or, if you'd like a free taste of what Property School is all about, watch one of our Property Investment and Education webinars, which are available online via live Zoom or on demand.

Happy Holidays and best of luck for 2021.

Property School gave me the best strategy for my situation and the motivation to act and do something. Real life examples and learning from speakers that are sharing experiences were highlights - Abha, November 2018

Gilligan Rowe and Associates is a chartered accounting firm specialising in property, asset planning, legal structures, taxation and compliance.

We help new, small and medium property investors become long-term successful investors through our education programmes and property portfolio planning advice. With our deep knowledge and experience, we have assisted hundreds of clients build wealth through property investment.

Learn More