Tax Changes and the Upcoming Election

5058POSTED:

Articles by Matthew Gilligan.

Lots of our clients are asking GRA what is on offer from the various parties for the 2023 election, so I thought it would be useful to recap the tax changes made by Labour in their past two terms, and then canvas the different offerings from political parties to reverse their changes. As a disclaimer, I’m not a fan of this government’s tax policy on residential landlords (being a landlord myself), so if you are left-leaning investor, you might be better to move on to another article.

When Labour astonished investors with bombshell tax changes in early 2021, I said that I would remind our clients and readers of the ‘about face’ the government did on tax policy in the run-up to the 2023 election. Let’s not forget Grant Robertson swore black and blue that the only tax change would be an increase in the top marginal tax rate to 39%. He said “no new taxes” but liberally interpreted that to meaning he could make huge changes to existing taxes, without campaigning on them transparently. He also very clearly said he would not extend the bright-line period, then he doubled it to 10 years.

Labour’s stated position on tax in 2020 election was not transparent

The most astonishing thing to me about the bright-line extension and interest non deduction rule changes, was the robust promise ‘set in stone’ from the Labour Finance Minister Grant Robertson in late 2020. You may recall the quite pointed Heather du Plessis-Allan interview, where she asked Robertson three times in a row to guarantee no tax changes other than increasing the marginal tax rate to 39%. Each time she asked him if he would change something, he said ‘no’; he was emphatic there would be no other tax changes and he certainly would not extend the bright-line period, he said. He made the same promise throughout the 2020 election as well.

I actually took him at his word; it never occurred to me he would back flip and make radical tax changes. More fool me (and others who take this politician at his word). Within 100 working days of taking office, Roberston implemented arguably the most far-reaching changes affecting residential property taxes in the history of New Zealand. In fact, Labour introduced the most radical new tax policy I’ve seen in my career as a chartered accountant.

Recap of the Labour tax changes

You will recall that in addition to Robertson demonising property investors with labels such as ‘tax evaders’, ‘speculators’, and the like, Labour set about changing tax policy to specifically target residential property investors, who are of course predominantly ordinary ‘mum and dad’ investors. These changes have included:

A few thoughts on these rules:

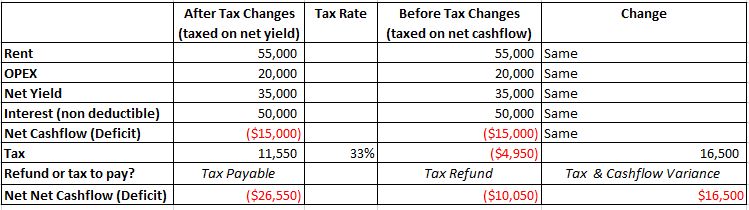

Looking at this example (that is endemic of what is going on in a higher interest rate environment for investors), if a residential property investor has $50k of interest cost and has negative cashflow of ($15k), they now get a $11.5k tax bill to pay. How is hitting someone with $15,000 of negative cashflow with a tax bill of $11.5k fair and equitable?

Remember, the investor also pays tax on the capital gain on the property if they sell within 10 years. And don’t forget new houses with Code Compliance Certificates issued on or after March 27 2021 don’t have to pay this tax (as new builds are exempt). This is distortionary, and crippling to smaller residential landlords who own second-hand houses, most of whom are small-scale landlords.

A Labour ‘Capital Gains’ tax for 2024?

I’m speculating here, but Labour have been clear in their messaging that while they want to see a wealth tax or full blown capital gains tax introduced into New Zealand, Jacinda Ardern said that it would not happen ‘while she was prime minister’. Well folks, she is no longer prime minister, and if Labour get a third term, I would bet my last dollar on a wealth tax emerging. But just as interest non deduction rules and bright-line rules are back-door capital gains taxes with different labels, I’m sure they will have a different label for a new wealth tax.

We have also heard through the traps that Labour are contemplating increasing marginal tax rates on high income earners. Mike Hosking among others was talking about it on radio. It’s all rumours and could be false, but I encourage you to think ahead about how this country is going to pay for all the costs that have been wracked up in the last six years, and who will pay for the increasing public expenditure from a well-meaning but very fiscally loose Labour-led government.

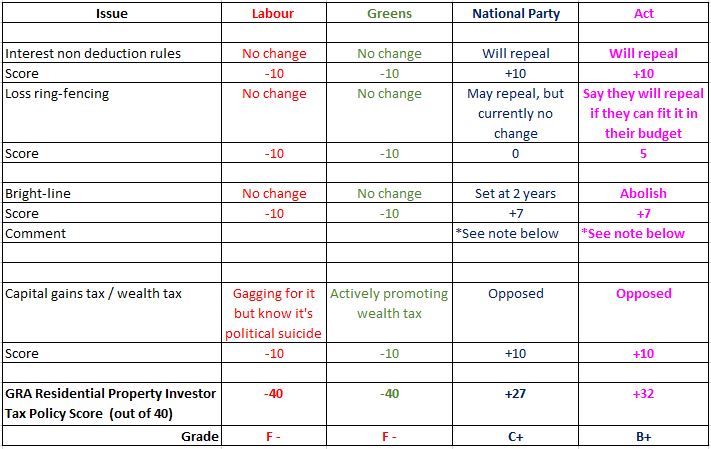

2023 Election Position of the Parties: Tax Changes

Below is a quick precis of the current stated position of from the left and right leaning political parties of New Zealand. I asked New Zealand First for their policy, but they had not responded at time of writing.

I’ll keep you updated if these policy positions change later this year.

Property Investors Tax Score of Party Tax Policy – by GRA as at March 2023

Act seem to be the most friendly to property investors’ tax plight; they get a B+.

Summary

It has been a rough ride for property investors under Labour. This government is attacking middle New Zealand with their property tax reforms, as it’s ordinary people being hit, not a tax-cheating landed gentry of wealthy property oligarchs (as the government rhetoric in 2021 implied).

Let us not forget the difficult to navigate residential tenancy rules rammed through this term, and the tinkering with LVRs and finance rules under the CCCFA shambles. It will be interesting to see if property tax becomes a significant election issue in the mainstream media for the 2023 election. I doubt it because there is no sympathy for property investors in the public eye. For residential property investors with debt, we know the interest non deduction rules are a hot election issue. That’s 50,000+ annoyed residential investors affected, all of voting age.

It remains to be seen whether Labour talk transparently about tax changes, and especially about wealth taxes. Meanwhile, I am pressing Act and National for their policy to improve on the loss ring-fencing changes that occurred. Their position on interest non deduction rules is excellent; these need to be reversed along with the other changes. I will keep you all informed as information comes to hand; David Seymour appears sympathetic to the property investors’ plight, and very responsive to policy queries. I encourage you to talk to your local National MPs about the issue – it’s worth impressing on our political contacts the importance to our part of the community of these tax changes being reversed.

More from GRA

For those of you interested in tax and legal structures, check out our blogs at www.gra.co.nz/#gra-blogs. I note we held a particularly popular webinar on Tax and Trust Structures that is trending, which you can watch at https://www.gra.co.nz/seminar-recordings/trusts-and-tax-webinar . For year end tax prepping and latest tax changes, you might like to have a look at https://www.gra.co.nz/seminar-recordings/year-end-prepping-update-webinar presented by GRA partners John Rowe and Anthony Lipscombe.

Property School gave me the knowledge, resources and confidence to seriously start looking at buying my first property in the next few months. All of the speakers had a wealth of knowledge (I rate them at least 12/10) - I've learnt so much! - Nerys Whelan, April 2019

Gilligan Rowe and Associates is a chartered accounting firm specialising in property, asset planning, legal structures, taxation and compliance.

We help new, small and medium property investors become long-term successful investors through our education programmes and property portfolio planning advice. With our deep knowledge and experience, we have assisted hundreds of clients build wealth through property investment.

Learn More