Auckland has peaked, but optimism still reigns in some of the regions, which are cycling two to three years behind Auckland. We have had a disruptive change of government, planning amongst other things to ban foreign buyers (for the most part), reduce immigration, and threatening with the green-eyed monster to tax the perceived lucrative property investor market more aggressively.

All of this is quite unsurprising really, and well predicted by many, including the writer. Each cycle has a clear pattern that seems to peak in Auckland in a seven year (1987, 1997, 2007, 2017), and if you have seen it before it's very familiar. Soon we will be in a downturn and our riches will diminish, public appetite to tax us will wane, and life will go on.

Changing Market Is now the time to hunker down and wait for better times to invest? Depends on what and where in my view – the different cities cycle behind each other (with ripple effect). You need to look at their fundamentals (supply vs demand and income levels of the city) and relative value to where they were in 2007, to make an informed decision.

I track this data quarterly at GRA as it is quite useful to assess where the regions and Auckland sit against each other, and what they did over the last cycle. I especially look at how much they devalued in the last down cycle to predict how volatile they might be in the next downturn. I don't like investing in areas that have a track record of devaluing as much as 20–50% from former peak value, as some areas did in New Zealand during the GFC post-2007.

Strategy Change for the Market Change In terms of strategy, if investors are still trying to employ old strategies that worked well during the boom phase of the property cycle, then their results are likely to be very disappointing as we move into the downturn. For example, while lowball offers did not work during the last few years, now lowball offers are the norm again in Auckland in the softer market, and are working.

My message here is when the property market changes and moves to a different stage in the cycle, you need to adjust your strategy. The trick is to

know which strategies work at the different phases the cycle passes through – and which strategies to avoid. I am continuing to invest in the current market, and the strategies many of GRA's clients and I are using at this time are producing great results. Have a look at the case study below, for a simple example.

CASE STUDY - Sunlands Avenue in Manurewa With a purchase price of only $540k, this subdividable 1128m2 property in South Auckland has a low entry cost, but stands to make an excellent capital gain. In an average Auckland area, with infrastructure already in place (due to a subdivision next door), how did I manage to secure it for such a low price?

The property had been on the market for over eight months and had been listed with several different agents with no success – mainly because the vendor's price expectations were absurdly high (they originally wanted over $800k for it which was $100k too much even at Auckland's peak in 2016). Probably one of those situations where the agent said “I'll get you $800k+” to get the listing, which has done the vendor a disservice on this occasion. (Sellers should be careful of agents high-balling the potential selling price to get listings. Go with the best agent, not the one offering the highest price.)

When I saw the property, the vendor had become more realistic, changed agent, and was asking for offers in the $600ks, so I offered $575k unconditional, as a cheeky offer. However, the vendor declined it because they simultaneously received a slightly higher offer of $580k, which was subject to due diligence. (Who would take the conditional offer for $5k more? This vendor did!) As luck would have it from my perspective, the other purchaser performed a meth test that came back slightly positive at +3. This scared them off, as they were home buyers, and they cancelled the contract. I was the backup buyer so the deal came back to me.

At this point I negotiated to reduce the price to $540k. (The contamination was only light, and I knew it could be remedied and retested for about $3-5k, using my own company to clean the house.) My offer was accepted, which was a bargain because other comparable properties of that size in the area are worth easily in the 600k's or early 700k's. We cleaned the house and it came down below the legal threshold, so that was easy. Amusingly we got one quote of $89,000 + GST to decontaminate the house. (They must have thought we were a government department!) We cleaned the house with a rag, rubber gloves and sugar soap for under $5k.

I settled this property into a joint venture I do a lot of development in (with a couple of mates). We are turning this single site into four titles and, including interest costs, it will require investor capital (our capital) of $625k. With a total cost of $2.35m (including land acquisition, funding, and house and development costs), it is projected to revalue at $3m – an equity gain of $650k. This means upon completion we will have basically doubled the equity we put into the deal with development margin. By not selling and instead renting the developed properties out, we do not pay real estate agent fees, GST or income tax. (There are specific tax exemptions from GST and income tax provided for developers who develop to hold.)

The net yield (both as a single site and after development) is around 4%, being rent - operating expenses as a percentage of cost. So this is not a cash flow strategy. If we don't build on it immediately, we will be getting capital growth on $3m (developed value), but our holding costs are on $540k. So the land bank element of this site is excellent. We stand to make $650k instant equity on the way in, if we develop the site. Lots of options here; we are in no hurry and will watch the market while we do the town planning.

These are the sorts of numbers and this is the sort of strategy that can make a big difference to your wealth over the longer term, a point lost on many investors who obsess over cash flow (because that is what they are told to do by their mentors). So while it's not a cash flow property, this is a great example of how you can create substantial capital gain in the Auckland market. I have more than 20 of these sorts of properties in my portfolio of 35 houses, because they create great growth over the longer term, and I don't have to develop them now – I can get the consents, or at least do the planning and queue them for when I perceive the construction, finance and political environment to be optimal, and then do the development.

Indicative design for Sunlands Ave development Cash Flow: Auckland vs the Regions

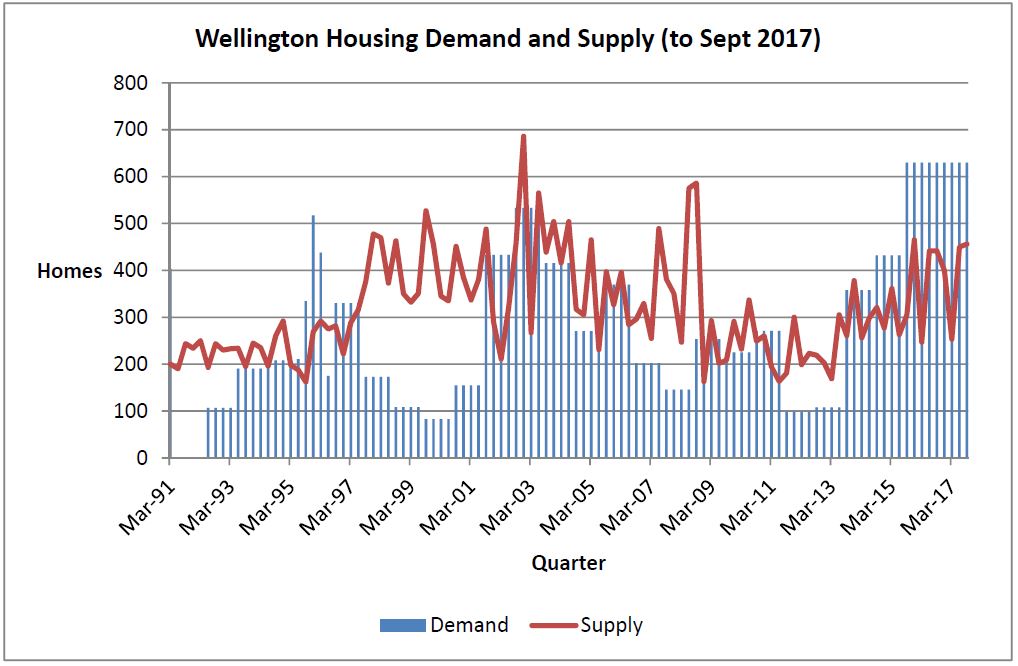

Indicative design for Sunlands Ave development Cash Flow: Auckland vs the Regions Investors have been flooding to the regions, which are cycling 1–3 years behind Auckland, and good cash yields are still achievable in some areas. In my view you need to be picky about your choice of area as mentioned above, because the regions are much more volatile and tend to crash further and for longer in a downturn. My pick at this point would be Wellington, because with Labour likely creating a large government requiring more offices and more people, there will be increased demand for property. Wellington has constrained property supply, as well as the highest average incomes in the country, so I would expect increased growth and better cash flow returns.

Wellington Supply vs Demand to Sept 2017

Wellington Supply vs Demand to Sept 2017

© Gilligan Rowe & Associates LP If I did not buy in Wellington, I would be looking in Hamilton which has a similar supply-starved look about it and high average incomes.

Auckland Cash Flow But what about in Auckland – is good cash flow possible in our largest city?

I personally have high cash flow properties in Auckland that are achieving more than 6%–8% net yields. These can be achieved in this market, but not from using standard buy-to-hold strategy – the numbers just won't stack up. To achieve this sort of return at this stage of the cycle (i.e. the peak of the cycle in Auckland), you need to use specific strategies, such as rent-by-the-room. Flat conversions are another very effective cash flow strategy that is working well at this time. Flat conversions are a new opportunity that has emerged under the Auckland Unitary Plan rules, allowing for a second dwelling within an existing property, provided basic criteria of 40m2 of internal space and 8m2 of private open space is achieved, along with meeting relevant building code. The cash flow flat conversions are comparable to minor dwellings, but much cheaper to build. This results in better cash flow than the old minor dwelling strategy investors have used in the past. Commercial property is also a good avenue for better cash yields.

When you marry high cash flow strategies (like the ones discussed above – there are more), with high growth in a property portfolio, you end up with balanced cash flow and some high growth assets. It's the high growth assets that will make you wealthy in the long term, but often they produce lower cash yields. Therefore, you need to be strategic – have high growth properties in half your portfolio and prop up their low cash flow with high cash flow assets in the other half. To understand the strategies that are effective, and how to change course as the market changes, take advice from experts who practice what they preach; educators who are walking their talk, who have substantial property portfolios, and who are actively investing.

At GRA we understand how important a good education is, which is why we regularly run our

free Property Investment Seminars as well as our

7-week Property School. If you like what you have read above, we invite you to come to Property School, where we discuss these sorts for strategies (we have lots of other strategies to share, too).

At GRA we are a team of enthusiastic property investors and accountants specialising in property, and we won't dazzle you will inaccurate numbers (that don't take the proper costs into account) or promote strategies that are ineffective in this market. So if you want fresh ideas that work in this market with an Auckland focus, attend one of our

free education evenings, visit our

website, or contact us on (09) 522 7955 or

info@gra.co.nz to find out more. Or check out some of my predictions and observations at GRA's

Seminar Downloads page.