Why you should split banks to take advantage of the loan-to-value (LVR) rules

5761POSTED:

Articles by Kris Pedersen.

While most of the attention recently around mortgage rule changes has concentrated on the implementation of the debt-to-income (DTI) rules, it is worth noting that on the same day this change came in (1 July 2024), the Reserve Bank also slightly relaxed the loan-to-value restrictions on secondhand investment properties.

Loan-to-value ratio (LVR) rules in New Zealand are restrictions set by the Reserve Bank to manage lending risks in the housing market.

They are the percentage of lending that a bank can lend against the value of the property they are taking as security.

For example, a $700k loan against a $1m property is a 70% LVR.

Key points about the current LVR rules

1. For owner-occupiers purchasing or leveraging property:

• Generally, a minimum 20% deposit is required, meaning a maximum LVR of 80%.

2. For residential property investors purchasing or leveraging existing property:

• A minimum 30% deposit is required, meaning a maximum LVR of 70%.

3. Exceptions and variations:

• First-home buyers may have access to lower deposit options, such as the Kāinga Ora First Home Loan with a 5% deposit.

• Some banks may offer low deposit options for first-time buyers with 5-19% deposits.

• New builds and construction loans may be exempt from LVR restrictions.

LVR changes over time

It is worth noting that the rules have been changed multiple times by the Reserve Bank since their introduction back in 2013.

The first LVR restrictions were implemented in October 2013 by Reserve Bank Governor Graeme Wheeler, aiming to slow house price growth, particularly initially in Auckland. However, these initial measures proved ineffective, as Auckland house prices continued to rise for the next three years.

In 2016, the restrictions were tightened, requiring a 40% deposit for secondhand investment properties in Auckland and 30% for the rest of the country. Over the following years, the Reserve Bank made several adjustments to the rules.

In April 2020 as part of the Covid-19 response, LVR restrictions were temporarily removed. This led to a significant increase in house prices as the country emerged from lockdown and throughout the rest of 2020.

The restrictions have been modified multiple times since their inception, with at least five changes occurring since 2020. These adjustments reflect the Reserve Bank's ongoing efforts to manage housing-related credit growth and house price inflation.

When you have multiple properties at one bank, the bank is limited to lending you against the collective security value.

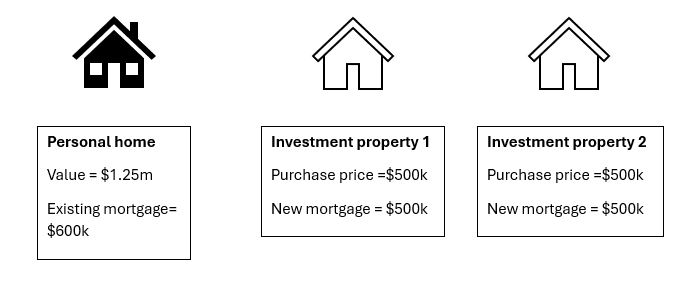

For example, let’s go back to when the Reserve Bank removed the rules in 2020 and it was possible to purchase existing investment properties at 80% LVR. Let’s say you had equity in your home, which had a mortgage at ABC Bank, and you decided to purchase a couple of investment properties. You would have ended up with a situation that looks like this:

ABC Bank

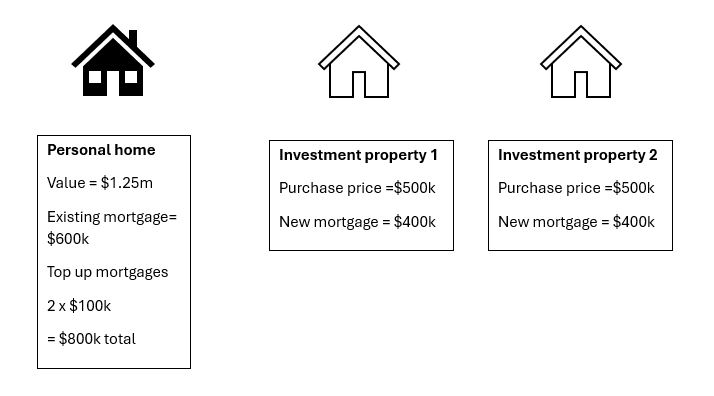

ABC Bank would have used equity in your home to enable you to purchase the two investment properties. Effectively what they actually did looks closer to the below because the equity in your home allowed you to top up your mortgage to the full 80% of value, meaning you had an extra $200,000 available for deposits on the investment properties.

When the LVR rules relax, the positive is that it becomes easier to leverage. However, the opposite applies when LVR’s tighten and if everything is held with one bank – it actually becomes harder to leverage.

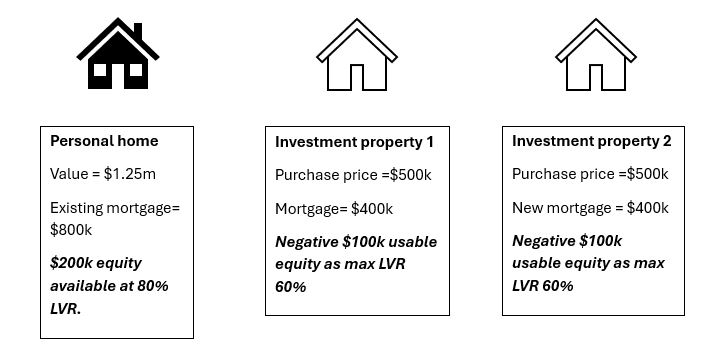

As we saw across 2021 when the rules tightened and it became possible to only leverage to 60%, and then 2022 to now when we have had a tighter property market which erased much of the growth from the low interest rate Covid market, the above investor will have ended up having a position which more looked like this:

In this case, the negative usable equity from the two investment properties offsets the available equity in the investor’s personal residence and they can’t do anything. At this stage they are limited to waiting for capital growth or non-bank solutions to invest further.

In other words, when properties are cross-secured, as illustrated in this example, you can end up with a negative usable equity position when the LVR rules became harder.

If, however, the investor had separated the investment properties to a different bank so that the only property held with ABC Bank was their home, then ABC Bank does not need to take the current negative usable equity position of the rentals into account because these properties are held by a different lender. Thus by split banking (having the rental properties with another bank), there would still be useable equity available in their home.

In this scenario, it is possible to go back and unlock the $200k equity that is in their home by leveraging it to 80%, and then bring in a further bank lender for the remaining funds to complete another investment purchase.

Besides the above clear benefit, there are also differences between banks as to how they asses a client’s maximum loan affordability. For these reasons, split banking opens up the ability to access further lending and potentially get another purchase across the line.

Key Recommendation

With the relaxing of investment loan-to-value rules, either now or when your fixed rates come off is the perfect time to make sure you benefit from the above structure.

If you would like to like to discuss this further please contact Kris Pedersen Mortgages HERE.

We want to thank you and your team for preparing these accounts for us. We have never been given such a detailed and extensive set of accounts in our lives! We’re very grateful and impressed with the amount of data you and your team have captured, deciphered and presented in such a professional manner. Thanks!

- Al & Michelle, September 2021

Investing in residential property?

If you're investing in residential property, seeking to maximise your ability to succeed and minimise risk, then this is a 'must read'.

Matthew Gilligan provides a fresh look at residential property investment from an experienced investor’s viewpoint. Written in easy to understand language and including many case studies, Matthew explains the ins and outs of successful property investment.